May 14, 2026

A friend of mine closed on a Fort Lauderdale canal home in 2022. Beautiful place — six bedrooms, infinity pool, deepwater dockage, the kind of view that justifies the asking price the moment you stand on the back patio. Eighteen months in, his seawall failed during a king tide. The repair came in at $94,000. His insurance covered none of it. His seller had pulled out of escrow on the seawall inspection contingency the previous year — and my friend, in a hurry to win the deal, had waived it.

Ninety-four thousand dollars to learn what an experienced waterfront buyer would have known to ask in the first thirty minutes.

This article is about those questions. It is not about how to find a luxury waterfront home in South Florida — your agent and the MLS will handle that. It is about what to do once you find one, before you become legally obligated to buy it.

The Mental Model That Saves You Money

Inland buyers think of a home as a structure plus a lot. Waterfront buyers should think of a home as four assets glued together: the residence, the shoreline protection, the marine structures, and the legal bundle of rights that connects all of it to the water. Each asset has its own condition, its own remaining useful life, its own permitting status, its own insurance treatment, and its own replacement cost.

When buyers get hurt, it’s almost always because they paid for one asset (the residence) and assumed the other three came along for free. They don’t. They come with their own price tags — sometimes invisible at closing, sometimes very visible eighteen months later.

The rest of this article walks through the four assets in the order experienced buyers actually evaluate them.

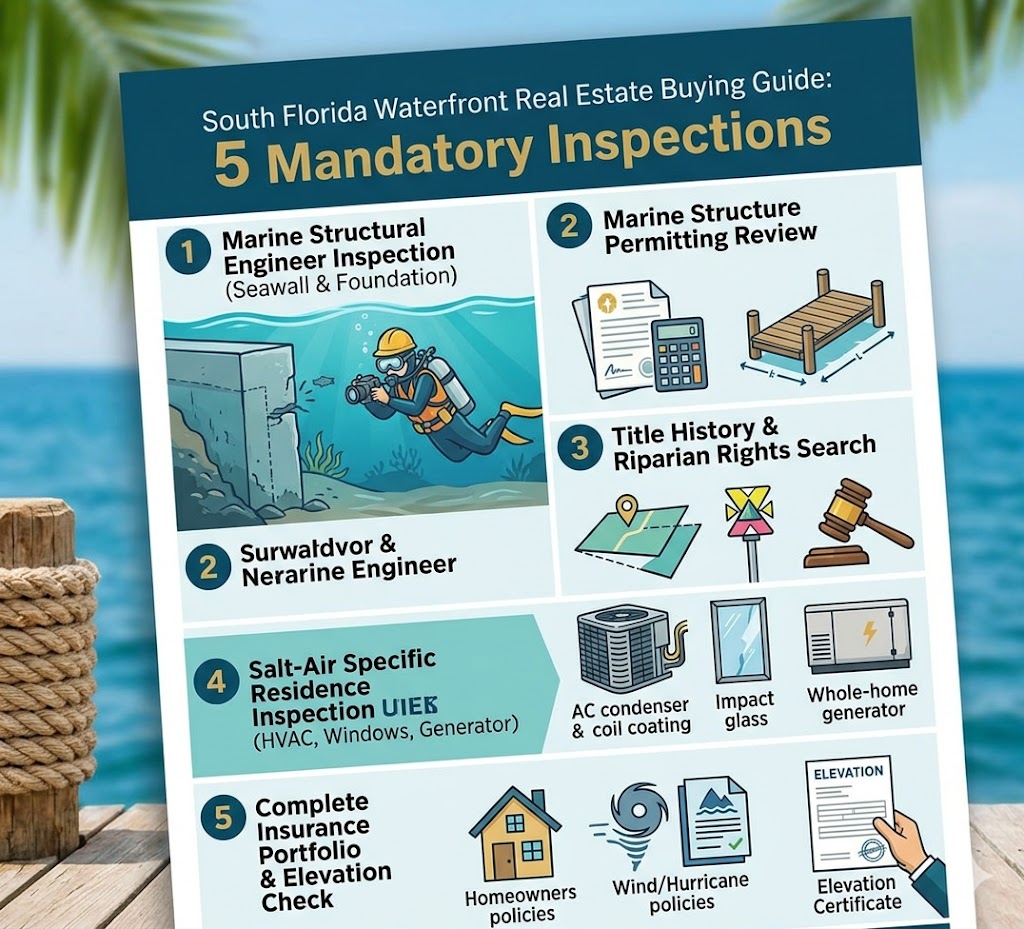

Asset One: The Shoreline Protection

The wall, bulkhead, riprap, or natural shoreline that holds the upland in place is, in most South Florida luxury submarkets, the highest-stakes piece of the property after the structure itself. Most existing seawalls were poured between the 1960s and 1980s. Engineering convention puts useful life somewhere in the 25-to-50-year range, depending on materials, original construction quality, water chemistry, drainage, and maintenance history. Do the arithmetic on a wall installed in 1972: it’s living on borrowed time.

Replacement is not subtle. Concrete and vinyl sheet pile installations in the South Florida market currently run in the neighborhood of $300 to $800 per linear foot, with engineering, permitting, and access logistics adding several thousand dollars on top. A 100-foot run on a typical Las Olas isle parcel can therefore land between $50,000 and $90,000 — and complications routinely push that higher. Properties with limited barge access, properties requiring environmental work, and properties needing elevation upgrades to current ordinance can run multiples of the baseline.

What experienced buyers do:

They retain a licensed marine structural engineer — the kind who carries a Professional Engineer seal — and order an inspection that includes both above-water and submerged evaluation. A divemask-and-camera inspection is now standard practice in Miami-Dade and Broward; it surfaces tieback corrosion, undercutting at the toe, and pile-cap separation that no walking inspection will find.

They ask whether the wall meets current ordinance, particularly NAVD88 elevation requirements that vary by county and have been tightened in recent years. A wall that’s structurally adequate but no longer code-compliant is a different cost picture than one that’s both.

They request maintenance documentation — weep hole servicing, prior repairs, cap restorations, tieback inspections. A wall with a documented history is a different asset than a wall with no records, even when they look identical from the dock.

They build a maintenance reserve into ownership cost projections. The seawall isn’t going to fix itself, no county program is going to step in, and the homeowner sits on the property line where the responsibility lives. Plan for it the way you plan for a new roof on a non-waterfront home — except more expensive and on a less forgiving timeline.

Asset Two: The Marine Structures

Docks and lifts look like recreational amenities. Legally, they’re regulatory artifacts. Three jurisdictions exercise authority over residential dock work in Florida — the U.S. Army Corps of Engineers (with most residential dock authority delegated to the state since 1998), the Florida Department of Environmental Protection, and the relevant municipality. A dock without a clean record across all three can be classified as an unlawful structure, and modifications to legally permitted docks frequently exceed what the original permit authorized.

The diligence isn’t complicated. It just has to actually happen.

Pull the permit file yourself, or have your attorney do it. A seller’s representation that “the dock is permitted” is worth less than a sheet of paper from the relevant agency. You want the original permit, every amendment, and the as-built survey. Compare what’s filed against what’s in the water — length, configuration, lift type, slip count. A 60-foot permitted dock now extending to 75 feet is a regulatory problem, regardless of whether anyone has noticed yet.

Confirm transferability. Some permits run with the structure; others require formal transfer or notification at closing. Your attorney handles this, but the question has to be asked.

Plan the future configuration before closing, not after. If the existing dock works for the boat you own, fine. If you intend to lengthen it, deepen the slip, add a covered lift, or accommodate a larger vessel, treat permittability as a precondition of the deal. The fact that your neighbor has the configuration you want is not evidence that you’ll be able to build it. Coastal Construction Control Line review, Environmental Resource Permitting, seagrass surveys, and submerged-land lease modifications can extend your timeline meaningfully — sometimes a year or more.

Check the electrical work. Modern lifts pull serious amperage; many older docks have undersized wiring or corroded marine connections that won’t pass insurance underwriting and create real fire risk. A licensed marine electrician should inspect the dock circuit during the contract period, not after closing.

For deepwater, no-fixed-bridge access, the dock can represent six figures of standalone value. For shallow or restricted-access locations, the dock can be functionally limited regardless of how it photographs. The difference matters and shows up in resale.

Asset Three: The Bundle of Rights

Waterfront ownership in Florida includes riparian rights — ingress, egress, dockage, an unobstructed water view, and reasonable access to navigable waters. The rights exist in statute and case law. They are not, however, automatic, unlimited, or guaranteed to be intact for any particular parcel.

The first question is whether the upland actually touches the water. The second is what’s recorded against the submerged land beyond the upland. Both deserve real attention.

A current survey identifying the mean high water line is non-negotiable. The MHWL is the legal boundary between privately owned upland and state-owned submerged land in Florida; it’s also the line above which the dock often must be supported and below which entirely different regulatory regimes apply. Surveys older than the most recent significant shoreline event should be redone.

Your attorney needs to look specifically for:

A hiatus parcel — a recorded gap, sometimes only inches wide, between the upland and the waterway. This is more common than buyers expect, particularly in older neighborhoods that have been re-platted or subdivided multiple times. A one-inch gap can extinguish riparian rights entirely.

Submerged-land leases. Some docks extend over land owned by the State of Florida and leased to the upland owner. Lease terms, renewal mechanics, transferability, and annual fees should all be reviewed and accounted for in the closing.

Recorded easements. Look for anything that affects view, access, or use — particularly utility easements that may constrain dock or seawall placement, and access easements that allow third parties to use the shoreline.

Accretion, erosion, and avulsion history. On bayfront properties and barrier islands, the legal boundary may have moved over the decades in ways that don’t match the visible shoreline today. A title history that doesn’t reconcile cleanly with the current condition is a yellow flag worth chasing.

Use a lawyer who actually closes waterfront. The trophy-tier brokerages in Miami, Fort Lauderdale, and Palm Beach all maintain referral lists; ask for one. The closing fees are a rounding error against the price of a rights problem you didn’t catch.

Asset Four: The Residence Itself, Adjusted for Salt

The home gets the standard inspection — roof, mechanical, electrical, plumbing, structural. What changes on waterfront is the diagnostic eye.

Salt air is corrosive and unrelenting. HVAC condenser units installed without coil coatings on a bayfront home will visibly deteriorate within a few years. Exterior hardware — door hinges, lift gates, gate motors, irrigation pumps, exterior light fixtures — has a shorter useful life than equivalent installations five miles inland. Window seals fail faster. Stucco needs more maintenance.

These aren’t reasons not to buy. They’re reasons to underwrite ongoing exterior maintenance as a meaningfully larger line item than a comparable inland property would carry.

A few specific items worth scrutinizing during the inspection period:

Impact glass and shutters. Insurance underwriting often turns on this. Older homes without impact-rated openings can face significantly higher hurricane premiums or, in some carriers’ models, decline-to-quote outcomes. Confirm what’s in place and whether it carries a documented impact rating.

Generator and electrical resilience. After Hurricane Irma in 2017, whole-home generators became standard equipment in luxury waterfront. If a property doesn’t have one, plan for the cost. If it has one, verify recent service records and fuel supply arrangements.

Pool equipment and waterfront irrigation. Saltwater proximity and frequent storm exposure batter equipment that inland buyers take for granted. Pool heaters, pumps, and irrigation controls all show their age faster on waterfront.

Foundation and ground-floor moisture history. Even properties that haven’t flooded may show signs of repeated water intrusion at the slab line. Look at baseboards, lower wall treatments, and ground-floor flooring carefully.

Respected South Florida Real Estate Developer Marc Elkman:

Marc Elkman Empire Development

Marc Elkman Florida Press Release

The Insurance Conversation Has Three Parts

Florida insurance had its worst period in living memory between 2022 and 2024. The picture is meaningfully better in 2026 — new carriers entered the state, rate-decrease filings took effect in January, and waterfront buyers can again get policies that two years ago they couldn’t get at any price. But “better” doesn’t mean “simple.” Luxury waterfront sits in the most underwriting-intensive segment of an improved market.

Three policies matter, and they don’t always come from the same carrier:

A homeowners (HO) policy covering the structure and its contents.

A separate wind/hurricane policy. Some HO policies include wind; many South Florida HO policies exclude it, requiring a separate windstorm policy from a private carrier or, when the private market won’t quote, from Citizens Property Insurance Corporation.

Flood insurance, written either through the National Flood Insurance Program or through the growing private flood market. NFIP coverage caps are low relative to a luxury home’s replacement cost, which is why excess flood policies are common at this price tier.

What experienced buyers do during the contract period:

They get bound quotes — not estimates — from named carriers, in writing, before the inspection period closes. The difference between a quote and a binder is meaningful, and the difference between a binder and a verbal estimate is enormous.

They request the FEMA flood zone designation and a current elevation certificate. AE versus VE versus X versus AO classifications materially change premium structure. A property elevated meaningfully above base flood elevation can qualify for premium reductions that change the ten-year ownership cost projection.

They confirm what’s not covered. Standard policies often limit dock coverage to nominal amounts; seawalls are commonly excluded as land improvements. Practically, the most expensive elements of the property may sit outside the insurance entirely. This isn’t a problem if you’ve priced the maintenance reserve correctly. It is a problem if you assumed insurance had your back.

They ask the agent for realistic three- and five-year premium trajectories. Florida premiums have stepped up sharply at renewal in recent years even on policies with no claims activity. Initial-year cost is a poor proxy for long-term cost.

If You’re Buying a Condo Instead of a House

A meaningful share of South Florida luxury waterfront is condominium product — Sunny Isles, Bal Harbour, Miami Beach, downtown Miami, parts of Fort Lauderdale, much of Palm Beach. The diligence sequence shifts.

Florida’s post-Surfside legislative changes mandate structural integrity reserve studies and milestone inspections for buildings of three or more stories, with timelines driven by building age and salt-water exposure. The intent is to surface deferred maintenance that low-reserve associations had been delaying. The effect, in many older buildings, has been to surface very large numbers.

Buyer questions in this segment:

Request and carefully read the most recent milestone inspection report and structural integrity reserve study. These are now standard buyer disclosures. Read them yourself, then have your attorney read them.

Examine reserve adequacy on a ten-year forward horizon. A building with substantial reserves and a small forecast capital plan is a different financial profile than a building with similar reserves and a large forecast plan. Look at funded reserves against projected concrete restoration, seawall work, elevator replacement, roof, HVAC, and façade.

Inquire about pending and recent special assessments. Anything assessed in the last 24 months should be priced into your offer. Anything pending should be priced into your offer at the high end of the estimated range, not the low end.

Look at operating budget structure. Some older buildings keep monthly maintenance artificially low and finance capital work through assessments. This makes individual units look cheap to carry until the assessment letter arrives. Higher monthly fees with full reserve funding is usually a more stable model.

New construction generally avoids these issues. The challenge concentrates in the older inventory between roughly $1M and $5M per unit — exactly the segment where the diligence work most clearly pays off.

Financing Notes

Most ultra-luxury waterfront closes in cash. The supporting tier — call it $3M to $15M — frequently uses jumbo financing, and the lender’s underwriting process will not move at the speed you’re used to from previous purchases.

Appraisal is the typical bottleneck. Genuinely comparable sales for distinctive waterfront properties are thin, and luxury appraisers experienced with unique waterfront product are not evenly distributed. Build extra time into the appraisal contingency, and ask your lender early which appraiser pool they use.

Lender insurance requirements may exceed your own. Lenders often want specific coverage minimums and policy structures; coordinate the insurance binder with the loan officer well before funding to avoid last-week surprises.

Self-employed buyers, foreign nationals, and buyers with complex income profiles routinely use bank statement programs, asset depletion programs, or interest-only structures at this tier. The right structure depends on your profile, but lining up the program before the property is found rather than after is the difference between a smooth closing and a stressful one.

For non-U.S. buyers, FIRPTA withholding, U.S. tax filing requirements, and the structuring decision (individual ownership versus LLC versus trust) all interact in ways worth working out with both U.S. and home-country tax counsel before signing.

The Offer Itself

A few moves that experienced buyers make and inexperienced buyers miss:

Build a realistic inspection period. Marine engineering, dock permit verification, title work specific to waterfront, insurance binding, and (for condos) reserve study and milestone review all take time. Twenty-one days is tight. Thirty to forty-five days is more honest for trophy waterfront.

Make the marine engineer’s findings a contingency, not just an inspection deliverable. The right to renegotiate or walk based on the engineer’s report should be specifically reserved in the contract language.

Negotiate seller representations specific to permits. The seller should warrant that the dock and seawall are permitted, with copies of permits provided at or before closing. This shifts risk and creates remedies if something turns up off-record.

Quantify and negotiate seawall and dock issues during the inspection period. Closing-table credits for known issues are a worse outcome than a renegotiated price with the issues priced in. Get the engineer’s repair-or-replace estimate in hand and trade on it.

Discuss enhanced title coverage with your title agent. Standard owner’s policies do not always cover waterfront-specific risks. Enhanced coverage or specific endorsements may be appropriate.

The Five Specialists Worth Having Lined Up Before You Tour

Buyers who do this well do not assemble the team after a property surfaces. They have it ready in advance:

A buyer’s agent whose deal book is heavy on waterfront. Not just any luxury producer — someone who has closed in the specific submarket and knows which seawalls in which canals failed last hurricane season.

A real estate attorney with documented waterfront title experience. Different practice area than a typical residential closing.

A marine structural engineer holding an active PE license. The signed report is the document everyone else’s analysis depends on.

An independent insurance broker who can shop multiple carriers, including the specialty market. Captive agents are limited to their own carrier’s appetite.

A Florida CPA. Homestead, snowbird domicile, foreign national considerations, and the federal estate tax exemption changes scheduled to land after 2025 all affect the right ownership structure for the property.

A Closing Thought

Luxury waterfront in South Florida remains one of the most distinctive asset classes in American real estate. Limited supply, sustained demand, irreplaceable geographic features, and a tax and lifestyle profile that continues to attract capital from higher-tax markets all argue for the asset’s long-term durability. None of that math changes the diligence math.

The buyers who do well in this market are not the ones who pay the lowest price. They’re the ones who underwrite the full picture — structure, shoreline, marine, rights, insurance, and maintenance — and pay the right price for the asset they’re actually getting.

Take the inspection period seriously. Hire the specialists. Read the reports yourself. Ask the questions sellers don’t volunteer answers to. The asset class rewards it.

Disclaimer (repeated): Educational content only. This article does not provide legal, tax, insurance, lending, or real estate advice and should not be relied upon as such. Cost estimates, regulatory references, agency processes, and procedural recommendations describe general practice and may not apply to any specific property or transaction. Permit requirements, ordinance provisions, insurance market conditions, and lender practices vary by property, jurisdiction, and time. Anyone considering a Florida luxury waterfront purchase should retain a Florida-licensed real estate broker with waterfront expertise, a Florida real estate attorney, a licensed marine structural engineer, an independent insurance professional, and a CPA familiar with the buyer’s specific facts. References to dollar amounts, agencies, products, or service categories are illustrative and do not constitute endorsement or solicitation.

About Brian French

This article combines human insight with tech-intelligent curation under our published Curation Protocols.Led by a commitment to tech-intelligent curation, Brian French tracks and analyzes Business News in Florida that defines Florida's economy. Brian brings an extensive financial background to his analysis, having graduated from the University of South Florida in Finance and serving as a Vice President and Portfolio Manager for Merrill Lynch Private Investors (a division of MLIM) and the Trust Department in St. Petersburg, FL, as well as a Vice President and Trust Investment Officer for SunTrust Bank in Sarasota, FL. His writing blends macroeconomic trends, capital markets analysis, corporate strategy, and modern digital insights for a sophisticated look at Florida's business news and economy.